Rare earth elements (REEs) are a critical group of 17 metallic elements essential to modern technology, renewable energy, and defense industries. Despite their name, they are relatively abundant but often difficult to extract in economically viable concentrations. China dominates the rare earth supply chain, controlling both mining and refining. This article explores the global distribution, demand, major industry players, China’s overseas investments, and efforts to reduce dependence on China.

--

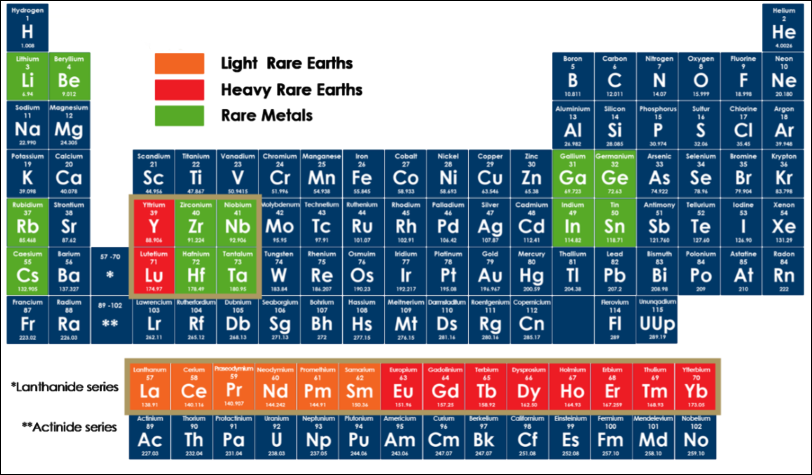

1. What Are Rare Earth Elements?

Rare earths consist of 15 lanthanides plus scandium and yttrium. They are divided into:

Light Rare Earth Elements (LREEs):

Lanthanum (La) – Used in EV batteries, optics, and catalysts.

Cerium (Ce) – Found in glass polishing, catalytic converters, and alloys.

Praseodymium (Pr) – Key for magnets, aerospace alloys, and fiber optics.

Neodymium (Nd) – Essential for permanent magnets in wind turbines, EVs, and headphones.

Promethium (Pm) – Radioactive, used in batteries and luminous paints.

Samarium (Sm) – Used in strong magnets, lasers, and nuclear reactors.

Heavy Rare Earth Elements (HREEs): (Scarcer and more valuable)

Europium (Eu) – Important for LCD screens and fluorescent lighting.

Gadolinium (Gd) – Used in MRI contrast agents and neutron shielding.

Terbium (Tb) – Enhances magnet strength in EVs and turbines.

Dysprosium (Dy) – Crucial for heat-resistant magnets.

Holmium (Ho), Erbium (Er), Thulium (Tm), Ytterbium (Yb), Lutetium (Lu) – Found in specialized optics, lasers, and nuclear medicine.

Related Elements:

Scandium (Sc) – Used in aerospace alloys.

Yttrium (Y) – Essential in superconductors, ceramics, and LEDs.

---

2. Global Distribution of Rare Earth Reserves

Rare earth elements are mined worldwide, but only a few countries have the refining capacity to turn them into usable materials.

Top Countries by Rare Earth Reserves:

China: 37% of global reserves, mainly in Bayan Obo (Inner Mongolia).

Vietnam: Large untapped reserves, increasing mining efforts.

Brazil & India: Significant reserves but underdeveloped infrastructure.

United States: Mountain Pass (California) is the largest non-Chinese source.

Australia: Mount Weld is a growing supplier.

Russia & Myanmar: Important suppliers but less influential in refining.

Why China Dominates the Market

China not only has vast reserves but also controls 85% of the world’s refining capacity. This is due to:

Early investment in REE mining & refining (1980s-90s).

Low-cost production, subsidized by the government.

Lax environmental regulations compared to the West.

Control over the supply chain (from raw ore to final product).

Western competitors struggle with high environmental costs, lack of refining facilities, and dependence on Chinese processing.

---

3. China's Overseas Investments in Rare Earth Resources

While China already controls a significant portion of global rare earth supply, it has also acquired stakes in reserves outside its borders to further strengthen its dominance.

Chinese-Controlled Rare Earth Reserves Abroad:

1. Greenland – Kvanefjeld Project

Chinese company Shenghe Resources has invested in Greenland’s Kvanefjeld rare earth project.

The project was suspended due to environmental and political concerns.

2. Myanmar – Rare Earth Mining Operations

Myanmar has become an important supplier of rare earths to China.

Many mines are controlled by Chinese interests and operate in regions with political instability.

3. Madagascar – Ampasindava Rare Earths Project

China Nonferrous Metal Mining Group has been involved in rare earth development.

Environmental concerns over its impact on Madagascar’s ecosystem.

4. Africa – Major Mining Investments

China has expanded its mining influence across Africa, securing key resources:

Democratic Republic of the Congo (DRC):

Chinese state-owned companies control 80% of the cobalt output, crucial for battery production.

Namibia, Zimbabwe, and Mali:

China has invested $4.5 billion in lithium projects, aiming to secure one-third of global lithium mining capacity by 2025.

Tanzania, Angola, Malawi, South Africa:

China is investing in eight rare earth projects expected to contribute 9% of global supply by 2029.

Zambia:

China is negotiating to rehabilitate the Tazara Railway, improving logistics for mining exports.

By controlling or investing in these projects, China ensures a steady supply of rare earths while maintaining its global market dominance.

---

4. Global Demand for Rare Earth Elements

The world’s rare earth oxide (REO) demand was 208,250 metric tons in 2019 and is projected to reach 304,678 metric tons by 2025.

Demand by Sector (2022):

Magnets: 44.3% (EVs, wind turbines, electronics).

Catalysts: 17.1% (automotive and industrial emissions reduction).

Polishing Powders: 12.1% (glass, optics, semiconductors).

Alloys & Metal Production: 9.3% (aerospace, defense, consumer goods).

Glass Additives & Ceramics: 11.7% (lasers, superconductors, coatings).

The growth of electric vehicles and renewable energy has significantly increased the demand for neodymium and dysprosium, with manufacturers seeking stable non-Chinese sources.

---

5. Major Chinese Companies in the Rare Earth Industry

Big Three Rare Earth Companies in China:

1. China Northern Rare Earth Group (CNRE) (600111.SS, Shanghai Stock Exchange)

World’s largest producer, specializing in light rare earths.

2. China Southern Rare Earth Group (State-owned, not publicly traded)

Focuses on heavy rare earths.

3. China Rare Earth Group (CREG) (State-owned, not publicly traded)

Formed in 2021 to consolidate China’s rare earth supply chain.

Other Key Publicly Traded Chinese Rare Earth Companies:

Xiamen Tungsten Co., Ltd. (600549.SS) – Specializes in tungsten and rare earth processing.

Shenghe Resources Holding Co., Ltd. (600392.SS) – Invested in global rare earth projects.

Jiangxi Copper Co., Ltd. (600362.SS, 0358.HK) – Involved in rare earth refining and copper production.

China strategically limits exports and imposes quotas, using rare earths as a geopolitical tool, restricting exports to Japan in 2010 and the U.S. during trade tensions.

---

6. Efforts to Reduce Dependence on China

Western Initiatives:

U.S.: MP Materials restarting Mountain Pass mining and refining.

Australia: Lynas Rare Earths developing non-Chinese processing facilities.

Europe: EU funding recycling and alternative magnet technology research.

Alternative Supply Strategies:

Mining Outside China: Investments in Vietnam, Brazil, and Africa.

Recycling REEs from electronic waste and old magnets.

Developing substitute materials to reduce reliance on REEs.

While efforts are ongoing, it will take years to break China’s monopoly due to its dominance in refining capacity and processing technology.

---

Conclusion

Rare earth elements are essential for the future of clean energy, high-tech industries, and defense. China’s grip on mining and refining has made REEs a strategic resource in global trade. With rising demand for electric vehicles, wind power, and advanced electronics, the world is urgently seeking new supply chains. While Western nations are investing in alternative sources and refining capabilities, China’s dominance will remain strong in the near future.

To secure long-term stability in rare earth supply, diversification, recycling, and technological innovations will be critical in reducing dependency on a single country.